CREDIT INSIGHTS

Alares Monthly Credit Risk Insights, April 2022

We received an overwhelming response last month to our Probuild case study.

This included a wave of new enquiries from credit providers, suppliers, builders, sub-contractors and advisors looking to better identify and manage their risk.

If you have a “top 10” list of customers, suppliers or key stakeholders that are causing concern, we have your back. Please get in touch to learn more.

This month we again take a closer look at the construction industry. While insolvencies are still below pre-COVID levels overall, construction related businesses are making up a larger percentage of those insolvencies.

Key highlights:

- Insolvencies in March were still slightly below pre-COVID levels.

- Construction related businesses are accounting for a larger percentage of all insolvencies.

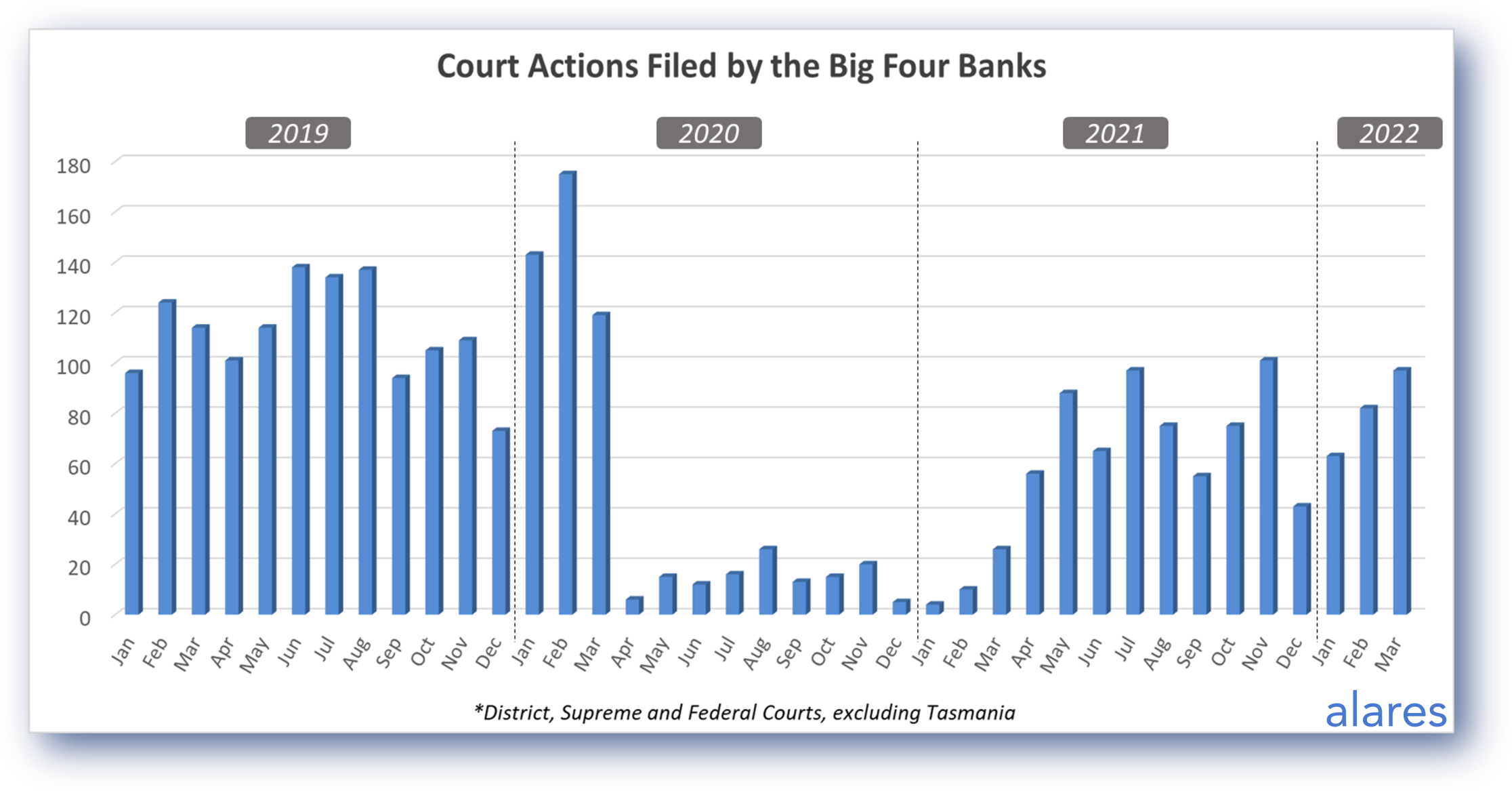

- The big four banks have steadily increased their Court recoveries since a lull in December. What impact will interest rates have in the months to come? And will this coincide with a more active ATO?

Insolvencies increased in March

March numbers were up on February but still slightly below pre-COVID levels.

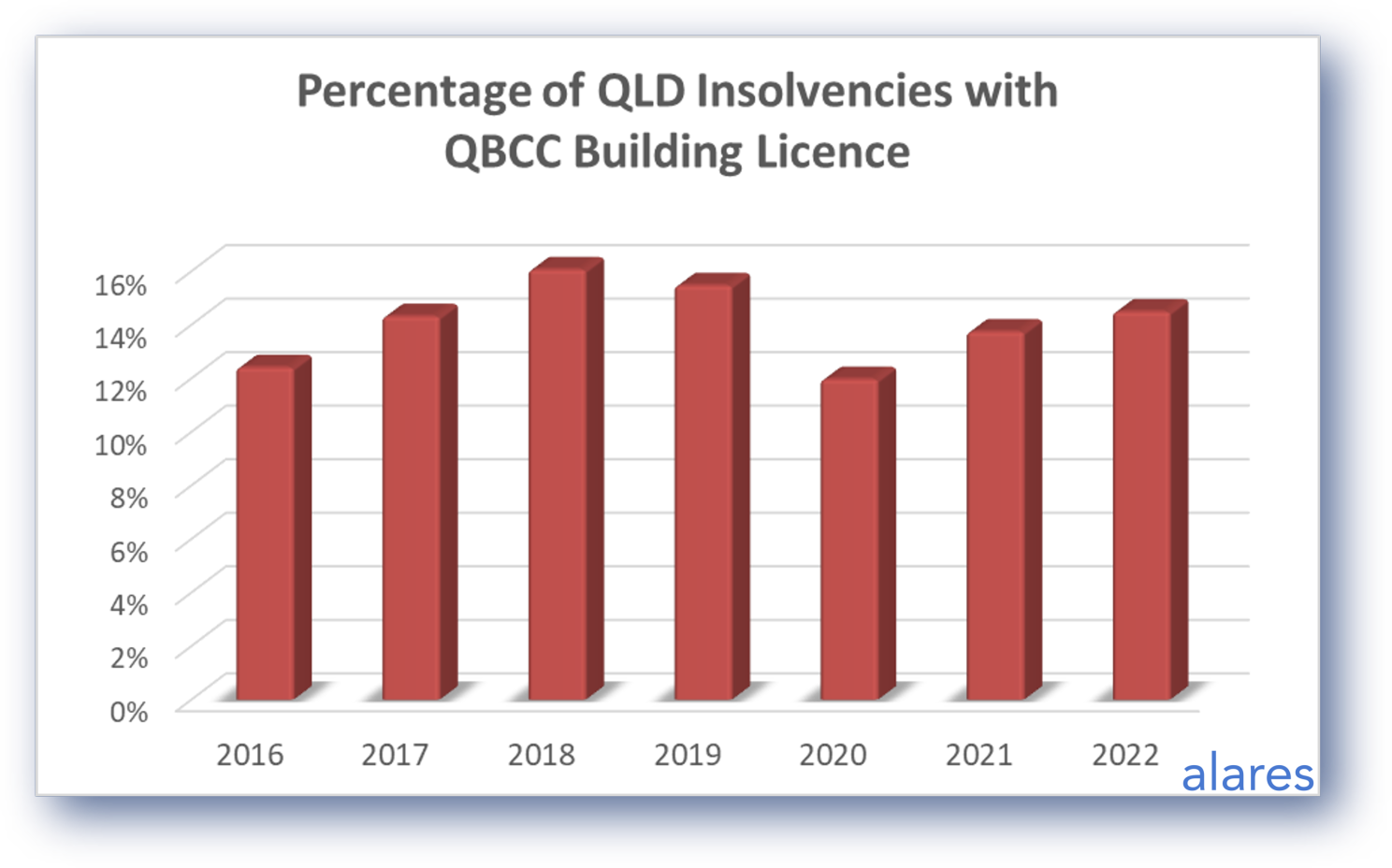

Construction related businesses are accounting for a larger percentage of insolvencies

As COVID restrictions eased over the last few months we saw fewer insolvencies for hospitality and tourism businesses, however transport operators and construction related businesses saw a steady increase in insolvencies.

The graph below shows insolvency data for companies with a building licence in QLD. Historically, QBCC licenced companies accounted for 12~16% of all insolvencies in QLD. This number peaked in 2018 before dropping off in 2020. The percentage has gradually increased in 2021 and 2022, and is again approaching the high of 2018.

The big four banks continue to remain active in terms of Court recoveries

The total number of Court recoveries initiated by the banks has trended up quite sharply since a momentary lull in December. The expectation for higher interest rates later this year will add to the pressure that businesses face in servicing their debts.

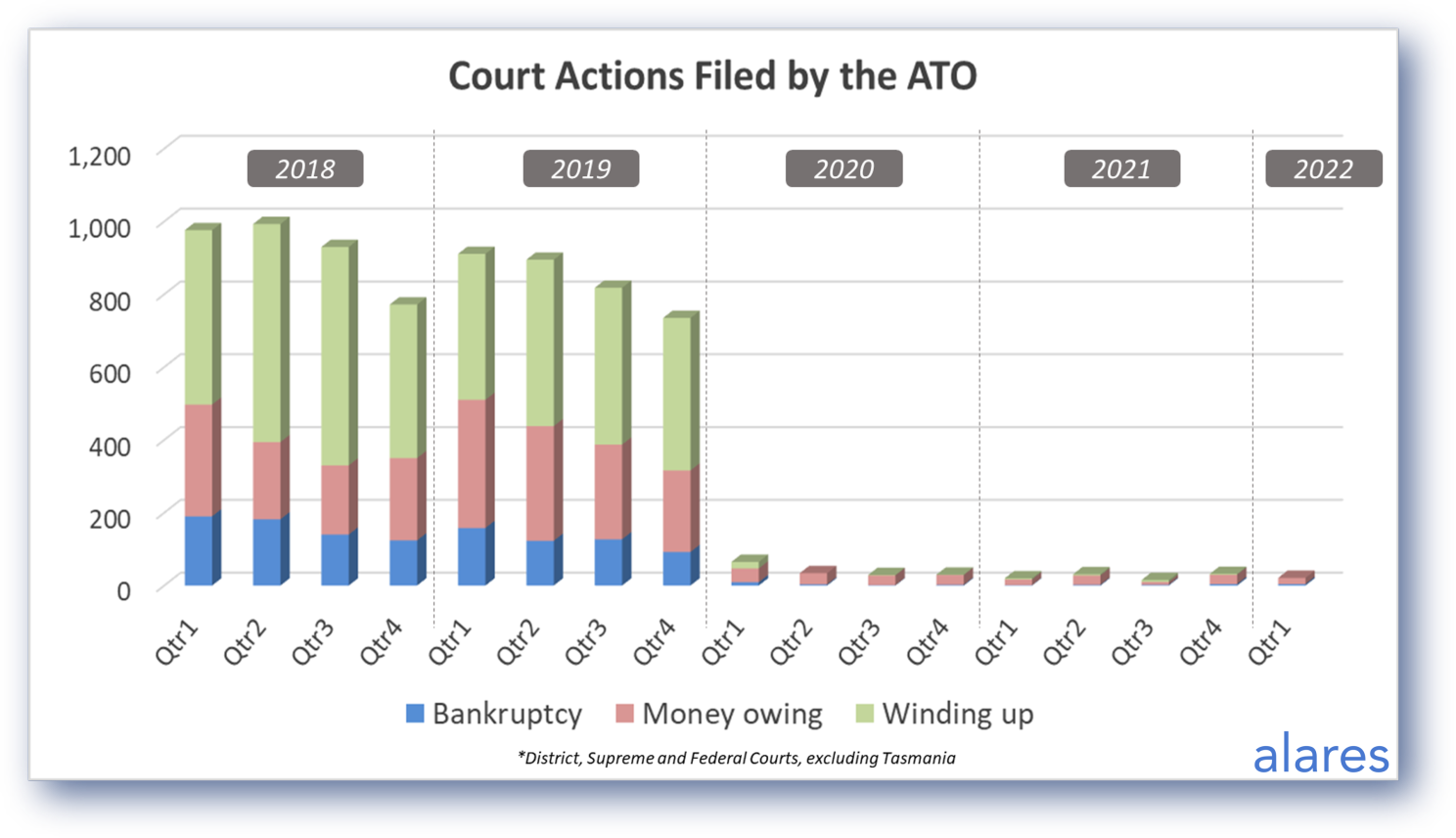

The ATO has remained largely inactive. Will a more active ATO also coincide with higher rates?

For its part, the ATO has stayed largely on the side-line since the onset of COVID. How big will the ATO debt bubble get before the ATO starts reengaging proper?

Many pundits have predicted a more active ATO in the second half of this year. We have already seen reports this week of warnings for imminent Director Penalty Notices. Will that coincide with higher interest rates to create a ‘double whammy’ for businesses that may already be struggling? Stay tuned for our future updates.

If you have concerns about credit risk relating to your customers or other key stakeholders, we are here to help

We work with businesses of all sizes across many industries. Our users benefit from critical data to help you make more informed decisions.

Act – Nov 2017")