CREDIT INSIGHTS

The HIA warns Australia’s housing construction downturn could get nasty unless credit continues to flow

- Australia’s Housing Industry Association (HIA) has warned that tighter lending standards risks exacerbating the downturn in residential construction activity already under way.

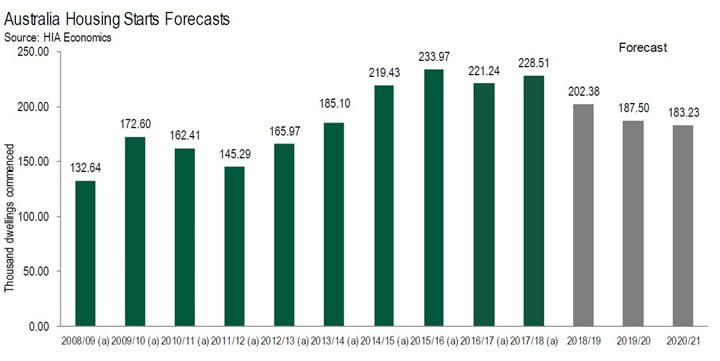

- The HIA is forecasting that housing starts will slow to 183,230 by the 2020/21 financial year, more than 50,000 less than the peak of 233,970 homes that began construction in the 2015/16 financial year.

- The construction sector is the third-largest employer in Australia behind healthcare and retail.

Australia’s Housing Industry Association (HIA) has warned that tighter lending standards risks exacerbating the downturn in residential construction activity already under way across the country, echoing similar concerns raised by Reserve Bank of Australia Deputy Governor Guy Debelle in a speech delivered last week.

Australia’s Housing Industry Association (HIA) has warned that tighter lending standards risks exacerbating the downturn in residential construction activity already underway across the country, echoing similar concerns raised by the Reserve Bank

“An unexpected tight squeeze on credit for home buyers is accelerating the slowdown in building activity,” said Tim Reardon, HIA Principal Economist.

“The credit squeeze that has been impeding investors for the past 18 months has expanded and is now restricting building activity across the market.”

In attempting to reduce what were, building financial stability risks from an increase in household debt levels, the HIA says the introduction of tighter lending standards since the end of 2014, seeing lending to investor, interest-only and high debt-to-income borrowers slow, may now be creating additional macroeconomic risks to the Australian economy by making the downturn in residential construction more severe than what would have otherwise been the case.

“APRA’s restrictions were designed to curb high risk lending practices but we are now seeing ordinary home buyers experience delays and constraints in accessing finance,” Reardon said, adding “the credit squeeze is weighing on a market that had already started to cool from a significant and sustained boom”.

“This disruption in the lending environment is impacting on the amount of residential building work entering the pipeline. The effect on actual building activity will become more evident in the first half of 2019.

“If these disruptions to the home lending environment prove to be long lasting then we could see building activity retreat from the recent highs more rapidly than we currently expect.”

And that includes for detached dwellings that have held up better than the downturn seen in apartment approvals over the past 12 months, falling by 2.7% compared to non-housing dwelling approvals which have slumped by 21.9%, according to data from the ABS.

“The year 2017/18 saw over 120,000 detached house starts,” Reardon said. “This is one of the strongest results on record.

“We expect new home starts to decline by 11.4% this year and then by a further 7.4% in 2019.”

As seen in the chart below from the HIA, housing starts could slow to 183,230 by the 2020/21 financial year, more than 50,000 less than the peak of 233,970 homes that began construction in the 2015/16 financial year.

Obviously, the group sees downside risks for these forecasts given the tighter lending environment for home buyers.

At a time when Australia’s population is growing at an annual pace of 1.6% per annum, according to latest demographic data from the ABS, Reardon has a blunt message to deliver ahead of the final report from Australia’s Banking Royal Commission early next year: keep credit flowing.

“With the prospect for the release of the Hayne Royal Commission’s findings to trigger further upheaval in the banking system, we need the banks to maintain stable lending practices for fear of a destabilising influence on the housing market,” Reardon said.

Not only could a more abrupt downturn in housing construction over this period create near and medium-term risks to the broader Australian economy, given the large number of Australians the sector employs, it could also lead to renewed affordability constraints for first-time buyers over the longer-term given continued strength in population growth.

In a speech delivered last week, Debelle said the biggest risk to the Australian economy from tighter lending standards was not the impact on households but rather property developers, especially in the new apartment sector.

Debelle said there was a risk that tighter lending standards for home borrowers could “lead to a sharper or more protracted decline in activity” in the residential construction sector.

“One risk is that tighter lending standards could amplify the downturn in apartment markets if some buyers of off-the-plan apartments are unable to obtain finance,” he said.

“This could lead to an increase in settlement failures, further price falls and even tighter financing conditions for developers.”

Such a scenario would likely lead to an even steeper drop in home building activity across the nation than the RBA and HIA expects, and likely create additional headwinds for employment, household spending and broader economic growth.