CREDIT INSIGHTS

Choppy waters ahead for the residential construction industry – this is a time to be vigilant!

As they say, ‘what goes up must come down’ and this is certainly true, at the moment, for the residential construction sector.

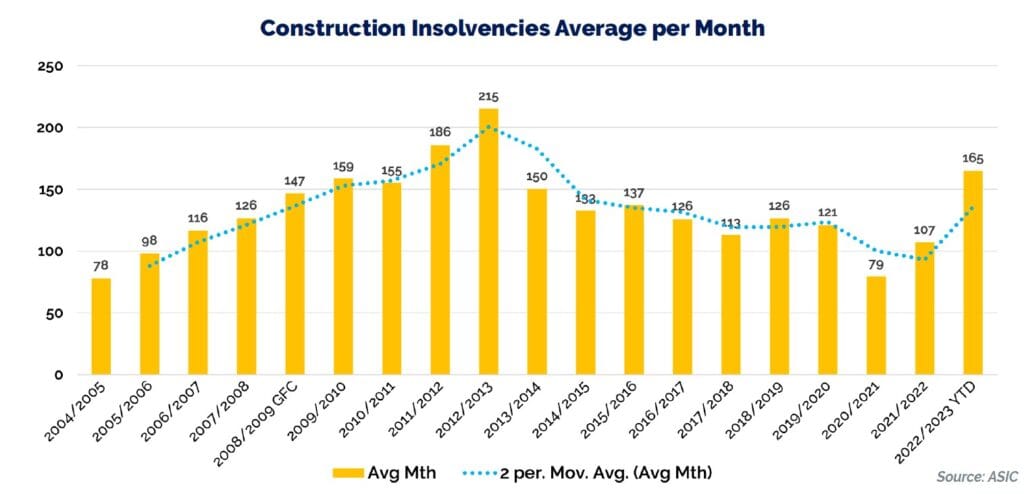

What a difference a year makes! This time last year, and despite a number of high-profile company collapses which sent shockwaves through the industry, overall insolvency numbers remained relatively low. Insolvency numbers fell quite sharply from June 2020 and remained relatively low until the second half of 2022. (see graph below). However, insolvency experts were warning that the construction industry was a “bubble waiting to burst”.

“Over the last two years builders have had to deal with a broad range of issues, from Covid-19 lockdowns, supply chain issues, severe weather events, rising material and wages costs and low profitability.”

Factors contributing to this elevated risk

Over the last two years builders have had to deal with a broad range of issues, from Covid-19 lockdowns, supply chain issues, severe weather events, rising material and wages costs and low profitability.

These issues have caused substantial blowouts in construction completion times, in many cases by as much as three months or more. Also, many builders on fixed-price contracts have made substantial losses. There is no doubt these issues are putting many businesses at risk. These factors have all contributed to what has been widely described as the “profitless boom”.

Overview of current risk in the building & construction Industry

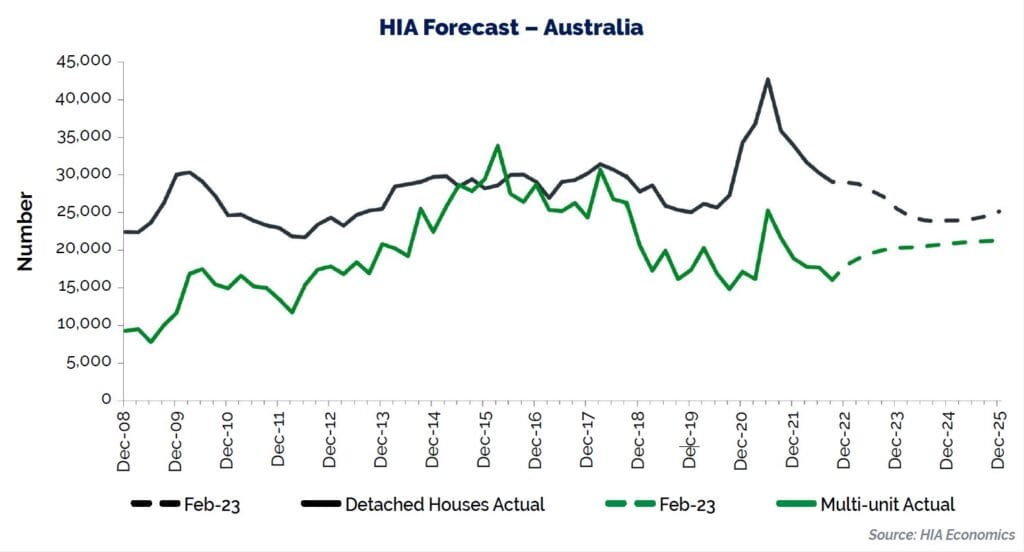

According to a recent HIA media release, the number of detached houses commencing construction is set to decline this year to its lowest level since 2012. This will see the number of detached housing starts fall below 100,000 starts per year for the first time in a decade to just 96,300 in 2024. This is a very rapid slowdown from the 149,000 starts in 2021. (HIA Media Release 21 February 2023)

This decline in the number of detached housing starts will generate a competitive pricing environment, particularly among the volume builders, in order to win work. This will ultimately impact their profit margins.

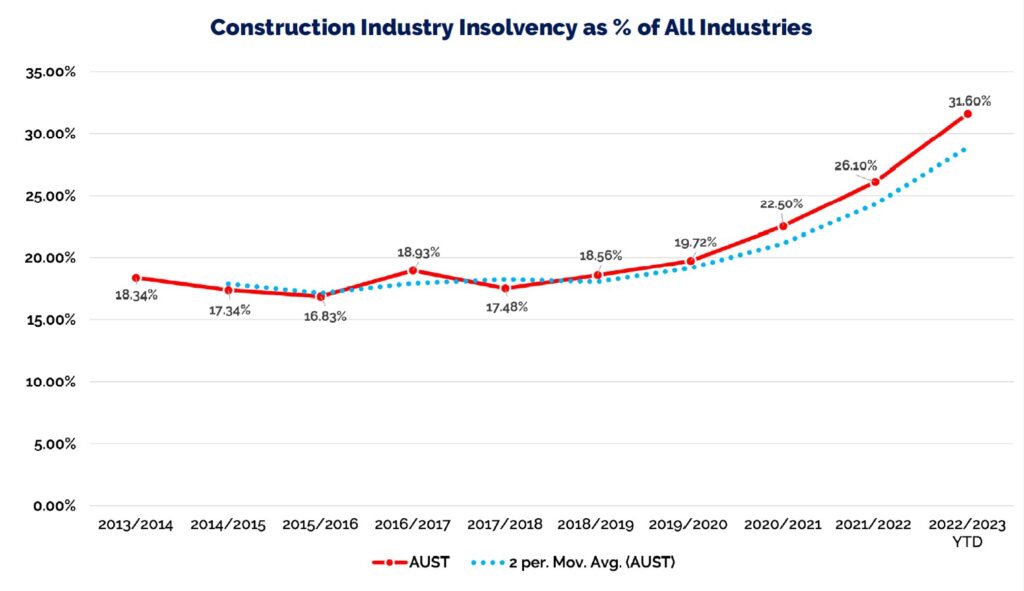

Construction industry insolvencies as a percentage of all insolvencies have increased by almost 12% (11.88%) during the Covid era. We expect to see that trend continue to increase over the next twelve months.

“Construction industry insolvencies as a percentage of all insolvencies have increased by almost 12% (11.88%) during the Covid era. We expect to see that trend continue to increase over the next twelve months.”

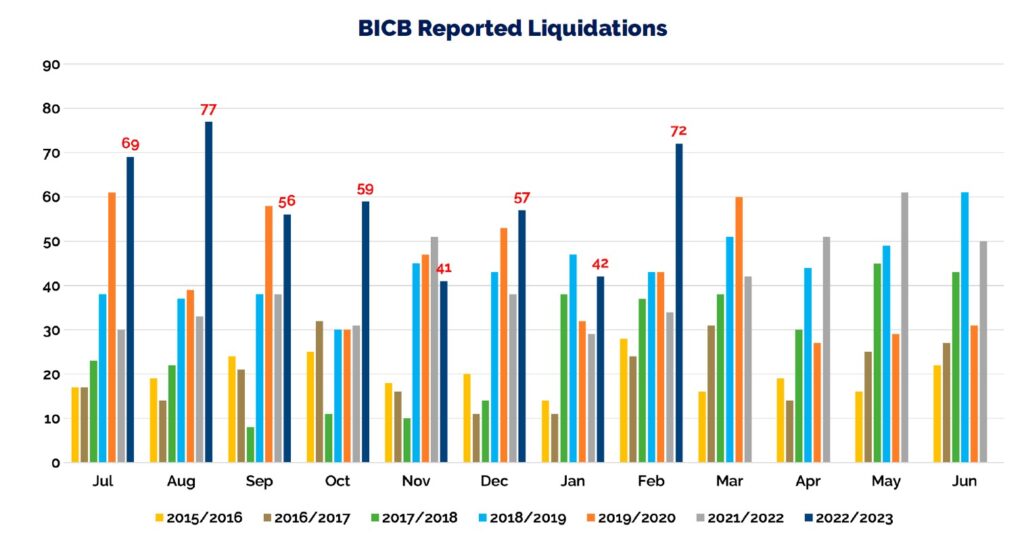

Construction industry insolvency forecast

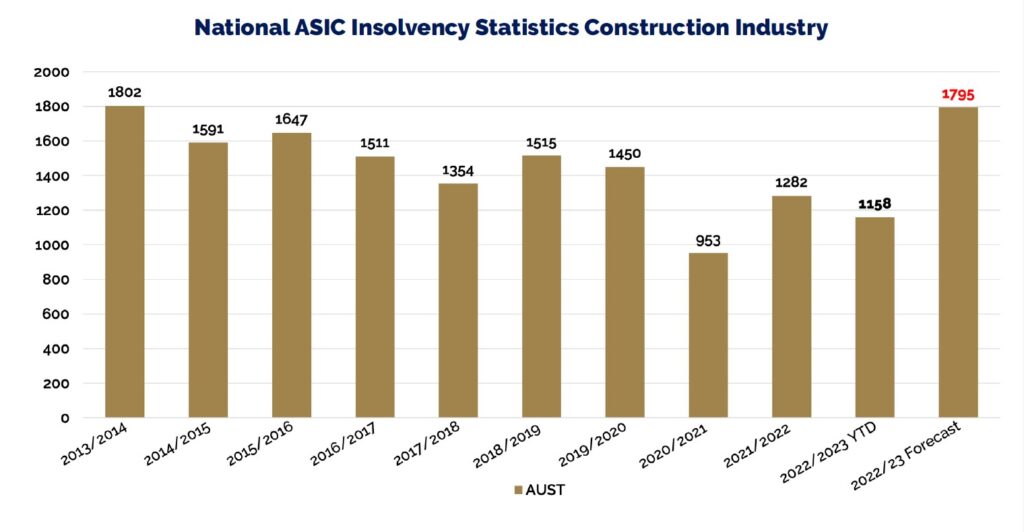

As can be seen in the graph below, insolvencies declined sharply during the Covid era. However, insolvency numbers for the current financial year are forecast by BICB to be the highest in ten years. (2022/2023 YTD to 31 Jan 2023).

BICB recorded liquidations for five of the past eight months, for entities reported in our database, have also been breaking records.

What is actually happening?

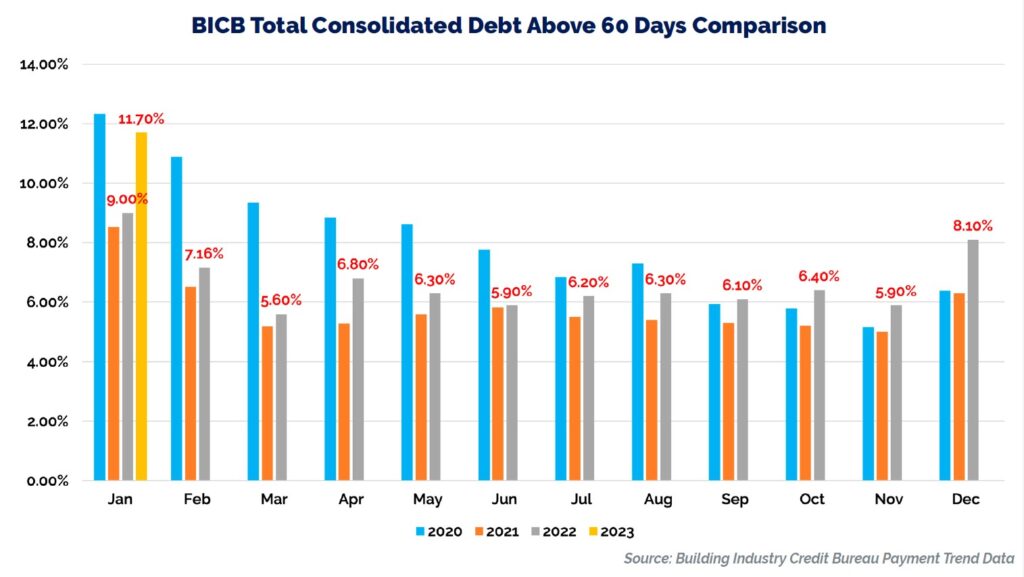

Debt Above 60 Days Trend

BICB’s data clearly shows how the debt percentage above 60 days decreased during the Covid era. However, recent feed-back from BICB members suggests that payments are beginning to slow down. This anecdotal information is reflected in the payment data for December 2022 and January 2023, above.

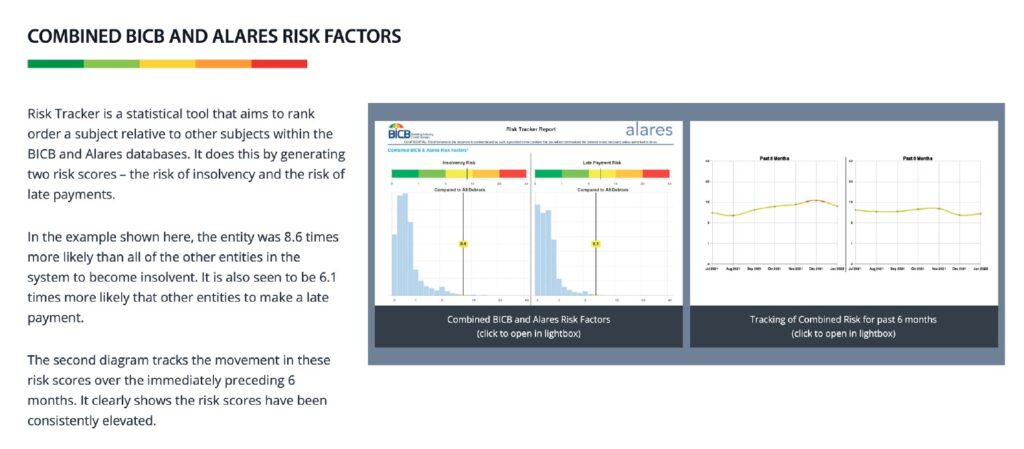

The value of data for successful risk mitigation

We live in a world where data is king. And with so much information available, the most effective risk mitigation systems will pull data from multiple different sources as no single source is able to provide the complete picture. However, for data to be useful in managing risk it needs to be accurate, comprehensive and, most importantly, early enough to provide advanced warning so you can be on the front foot to mitigate your risk in real-time. Some data sources are retrospective in nature and provide great clarity after the fact, but these have limited value as situations evolve. Fortunately, there are a number of other excellent tools available to credit managers that can identify deteriorating trends and potential red flags months in advance of eventual business failures. Use of these tools within your credit management processes can add significant value to your business.

“…for data to be useful in managing risk it needs to be accurate, comprehensive and, most importantly, early enough to provide advanced warning so you can be on the front foot to mitigate your risk in real-time.”

“Assessing any customers’ credit risk profile is only possible with access to data that is comprehensive, accurate and up-to-date. ‘Credit Risk Management’ techniques and models that are supplied with rich data sets will help significantly improve credit risk processes.”

This is a time to be vigilant

Know Your Customer – Front and centre of managing your risk is having a strong understanding of your customers. This is essential for any business looking to succeed in creating reliable credit risk management processes.

Assessing any customers’ credit risk profile is only possible with access to data that is comprehensive, accurate and up-to-date. ‘Credit Risk Management’ techniques and models that are supplied with rich data sets will help significantly improve credit risk processes.

Assessing Risk – Whether onboarding new customers or, reviewing existing customers, access to meaningful data is critical. This information is generally sourced through Credit Reporting Agencies and Industry Trade Bureaus that provide online access to current and historical trading data, comprehensive Court action reports and alerts, ASIC data, Licencing Regulators and Trade References from other suppliers. Both of these sources provide their own unique valuable data to feed into a comprehensive risk management process that enables the credit team to make the most informed decisions.

As an example BICB members have the advantage of having access to large sets of trading data which enables them to monitor payment trends.

If you would like to see how BICB’s data can benefit your business, please Book a Guided Tour. Through this Zoom meeting, you will be guided through BICB’s user-friendly systems and view the in-depth data. This meeting is free. Joining BICB could potentially save you thousands.

Wayne Clark MICM, MAICD

Executive Director, Building Industry Credit Bureau

E: wayne@bicb.com.au

T: 0402 244515

Acknowledgements

(a) Graphs supplied by Building Industry Credit Bureau